MONTHLY NEWSLETTER – MAY 2026

June 1, 2026 |

Download Document

A summary of key events and market trends during the month of May

Global Markets Updates

- After a difficult six months for software stocks, the opportunity set looks more attractive. The sell-off has compressed multiples in many high-quality names just as the underlying demand picture is beginning to broaden beyond experimentation. Customers are moving from pilots to production, budgets are being reallocated toward automation, data infrastructure, cybersecurity, and workflow software, and AI is making software more valuable rather than less relevant. The key distinction now is between companies with durable distribution, embedded workflows, and pricing power, versus those merely adding AI features. For patient investors, the reset has created a better entry point into long-term compounders.

- Kevin Warsh’s confirmation reinforces an important shift in the macro debate: productivity is moving back to the center of monetary policy. His recent dovish comments reflect the view that the AI boom could prove highly deflationary over time, as businesses use automation to lower unit costs, improve labor efficiency, and expand output without equivalent pressure on wages and prices. That does not mean inflation risk has disappeared, but it does suggest the Fed may have more room to ease if productivity gains become visible in the data.

- The broader US growth picture remains healthier than the headline debate suggests. AI and related technology spending are no longer confined to the mega-cap technology complex; they are beginning to stimulate activity across power, industrial equipment, data centers, semiconductors, consulting, software services, cybersecurity, healthcare workflows, logistics, and financial services. This matters because technology cycles become more durable when they pull adjacent sectors into the investment wave. The capex boom around compute, energy, and infrastructure is creating second-order demand across the economy. While some areas remain cyclical, the US retains a powerful combination of innovation, capital depth, and entrepreneurial flexibility.

- Over the next two to three years, AI is likely to move from model spectacle to practical deployment. The frontier will still matter, but the bigger commercial opportunity may come from agentic workflows, enterprise automation, domain-specific models, inference optimization, robotics, edge AI, and better integration with existing software systems. The winners are likely to be companies that reduce cost, latency, and complexity while making AI reliable enough for regulated and mission-critical use. We should expect fewer vague AI promises and more measurable productivity outcomes. The market will increasingly reward execution, distribution, infrastructure advantage, and real customer ROI.

Navigating Tech Positivity with Geopolitical Negativity

The overall month-by-month narrative does not seem to see much alteration in 2026

We believe the trends in technology are well established and will only continue; price action here while positive will see some choppy times

Key Markets

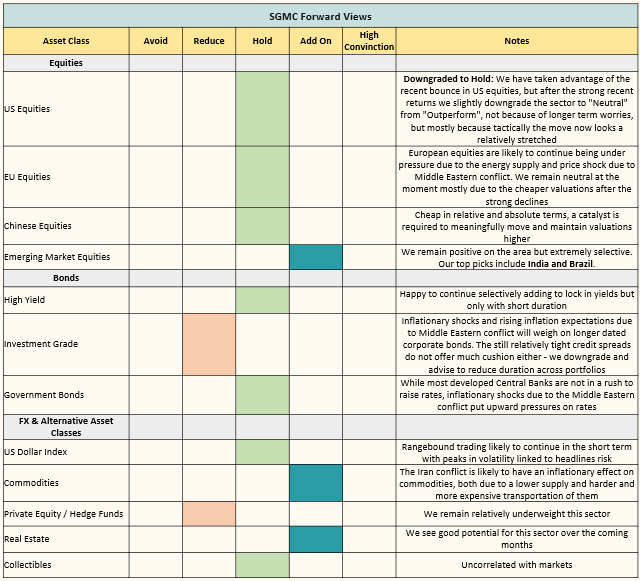

SGMC Forward Views …

- Downgraded US Equities from Add On to Hold: We have taken advantage of the recent bounce in US equities, but after the strong recent returns we slightly downgrade the sector to “Neutral” from “Outperform”, not because of longer term worries, but mostly because tactically the move now looks a relatively stretched