MONTHLY NEWSLETTER OCTOBER 2023

November 1, 2023 |

Download Document

A summary of key events and market trends during the month of October

Global Markets Updates

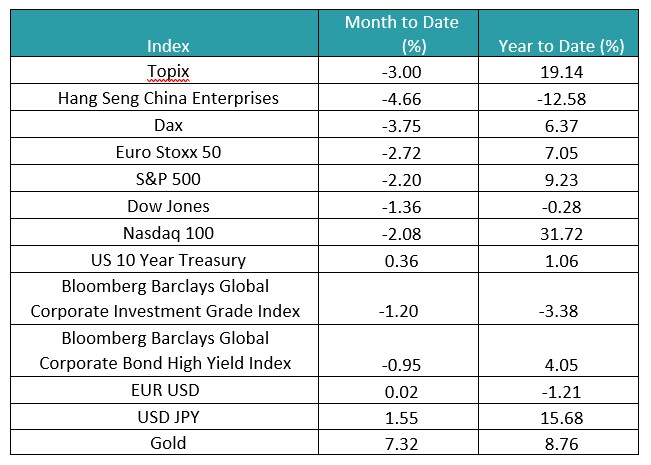

- Global equity markets have lost somewhere between 8 – 10 % of their value since the highs in July. The S&P 500 and the Nasdaq are down around 8.6 % while the Dax has done marginally worse at down 9.8 %.

- In a continuing fashion, China has managed to underperform once again with the Hang Seng China Enterprises Index down around 15 % in the same period.

- President Biden and President Xi are scheduled to meet in San Francisco in November and any constructive dialogue will be welcomed by global investors.

- The Federal Reserve met yesterday and with the economy and employment continuing the strong momentum and inflation decelerating they indicated no desire to hike nor cut rates in the short term. This has been our long-held view, and we expect the Fed to be on hold for the next few meetings.

- The employment numbers need to be watched closely as very often they are a lagging indicator of economic activity and any developing softness here could indicate that the economy is already heading onto a slower path.

- The Bank of Japan continues to indicate no desire nor intention to normalize policy like its global peers have. In his comments yesterday Governor Ueda referenced weak inflationary pressures in the out years despite stronger than desired inflation in the short term. The Japanese Yen has weakened to 150 per US Dollar and we see increasing chatter of FX market intervention.

- The situation in the Middle East led to a brief spike in the Volatility Index (VIX) to over 20 and, while we watch this closely for signs of building investor unease, has now settled below that important pivot level.

Markets continue their holding pattern

Developments in the Middle East and the interest rate outlook have, for now, reduced the appetite for risk assets.

Key Markets

- The Biden Administration continues to develop plans to help develop broad swathes of the US economy. From the initial infrastructure spending to the CHIPS Act to hydrogen facilities being built out, the focus now is on developing over 30 technology hubs across various states. While the funding for the latest endeavor comes from earlier programs it demonstrates the process of investing in growth areas that has now become a consistent theme. The multiplier effects of such investments lead to stronger growth down the line and will likely temper any weakness on account of the drag from higher interest rates.

- Hang Seng continues its yearly underperformance, with the divergence from Nasdaq now at a staggering 44%. Only a substantial and concerted effort from the government and local central bank, as well as increased visibility for business developments, will be able to finally lift this market from depressed levels

- European equities have recently underperformed their American counterparts as we expected, we believe this trend has more room to go

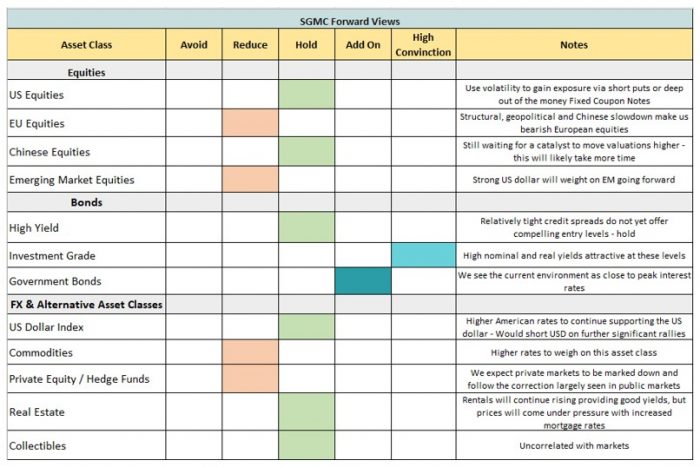

SGMC Forward Views …

- We upgrade Investment Grade bonds to High Conviction as the risk reward across the curve looks compelling. We anticipate the possibility of gains over the next 12 months coming mainly from duration as well as tightening spreads for higher quality issuers.