MONTHLY NEWSLETTER OCTOBER 2022

November 1, 2022 |

Download Document

A summary of key events and market trends during the month of October

- October has seen investors holding cash deploying the same into risk assets at relatively attractive levels. This has put a bid under prices at lower levels and we would expect the lows of the year to hold barring major geopolitical escalations

- China held its 5 yearly Communist Party Congress and President Xi has consolidated his control by nominating allies into key appointments. This has important investment implications which we delve into detail in the following page

- Inflation readings continue to be high across most economies and while goods inflation has been muted and lower, services have continued to be resistant to higher rates

- In the US rental prices are the key element which we expect to now soften over the coming months

- The Dollar has seen some pause in its rally across most majors and we expect other Central Banks to hike proactively under cover of the Fed’s hawkishness

- As we had anticipated markets have rallied from the lows and buying interest keeps kicking in at depressed levels

- Geopolitics continues to be an active issue that market participants focus on with multiple moving parts in various spheres of influence

- This keeps the Volatility Index well bid at the lower end, while relatively reasonable valuations ensure that we are not testing previous highs

Closer to a pause?

Not so fast … we expect the Federal Reserve to continue hiking rates over the coming quarters albeit at a slower pace

The US and global economies are feeling the pain from the sudden reversal of easy policy and while the Fed has done a good part of the heavy lifting we are not close to a pause in the fight against inflation

Key Markets

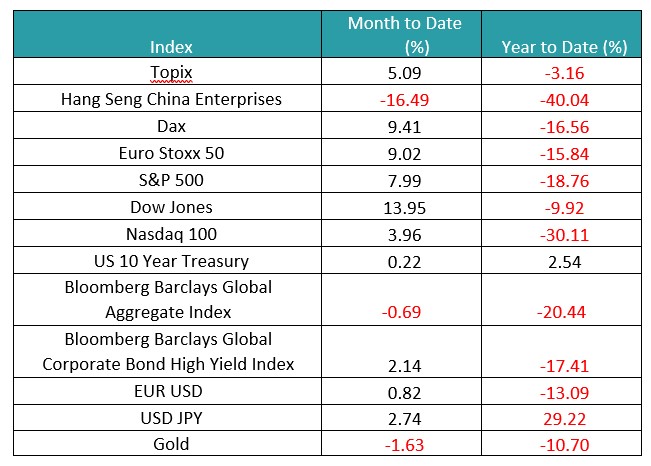

- October has provided some relief for investors with markets testing the years lows but holding well for now

- Year to date markets are still deeply in the red but with the Federal Reserve now indicating that the heavy lifting on interest rates may be out of the way we could see support build up at lower levels

- The USD continued to see appreciation but in line with the bounce in equities has sold off from its peak

- European equity markets have also found a bid; however, we view that as temporary as the continuing war and related concerns will likely cap further rallies

- Fixed income markets now present themselves as strong alternatives given the yields available and we have started increasing exposure to good quality credits

20th Chinese Party Congress Update

- The much awaited 20th Party Congress has concluded and the leadership team has been revealed

- Xi Jinping has further consolidated his hold on power. The extent to which he did significantly exceeded expectations, based on most of the political analysis heading into the meeting

- From a political perspective, some observers are characterizing the 20th Party Congress as the most surprising in decades. The focus on Taiwan brings this specific geopolitical risk to the fore

Some perspective:

- All four newly-announced PBSC (Politburo Standing Committee) members were largely considered outside chances for elevation to the body heading into the meeting. All four are Xi allies.

- Surprising retirements – Wang Yang and Li Keqiang (current Premier). Both would have been eligible for continued service on the PBSC. Most expected some continued senior role for Li Keqiang and Wang Yang as a base case and placed a low probability on full retirement given their age.

- Surprising promotion – Li Qiang, now the most likely next Premier replacing Li Keqiang in March 2023. He will be the second most powerful figure in China. He is the Party leader in Shanghai. Many thought the COVID outbreak in Shanghai earlier this year would have reduced or doomed his chances at promotion. His elevation provides the latest indication that political loyalty outweighs economic performance under Xi.

- If there was any doubt about Xi’s political standing within the Party or State, as had been frequently speculated over the past year, the 20th Party Congress was an emphatic display of not only Xi’s ongoing control over the Party, but also his strengthening position within it.

- While the most important short-term implication of the 20th Party Congress is in simply getting it out of the way we believe there are a number of important medium to long term themes coming out of the 20th Party Congress

- the near-term focus will likely shift to restoring a stable economic environment.

- We do not see China abandoning its Zero-COVID approach in a wholesale manner, but we do think risk tolerance for incremental changes to COVID policy will go up following the meeting.

A few themes stand out at the moment:

- Heightened urgency around Technology Self-Reliance

- A more insular country and economy which further confounds supply chain issues that the world is dealing with

- A more aggressive stance towards Taiwan raises the ante on geopolitical risks in the region and globally

- From a financial point of view, the outcome of the Party Congress was negative, as it further increases geopolitical risks within the Asian region, as the strong consolidation of power under one leader adds uncertainty

- This was clearly visible in the market reaction: the Hong Kong stock exchange lost over 16% in the month of October alone

- Going forward we expect volatility and uncertainty to remain, but barring an escalation related to Taiwan current Chinese equity valuations are too cheap to ignore

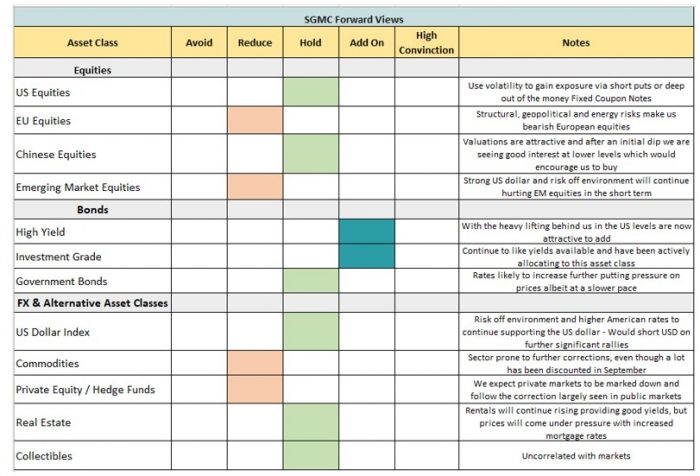

SGMC Forward Views …

- While the June lows were tested they managed to hold over the months of September and October. We would expect these to hold barring any major negative geopolitical developments.

- The November Federal Reserve meeting has priced in a further hike of 75 basis points and investors will be looking at comments on the future outlook of policy this week

- Next week the US elections will be keenly watched for the shape of the new Congress and we will await results before adjusting our views accordingly

- We continue to prefer American equities as compared to European as the energy situation, while under control in the short term, will likely be a drag over the medium term