MONTHLY NEWSLETTER NOVEMBER 2023

December 1, 2023 |

Download Document

A summary of key events and market trends during the month of November

Global Markets Updates

- Heading back to highs of the year has been the theme for equity markets in the month of November. The, oddly constructed, Dow Jones Index has pushed through to new highs and now most have the early 2022 levels in sight.

- China, on the other hand, continues to feel the compounding weight of its policy decisions and the China Enterprises Index trades at close the year lows.

- Expectations of a détente between the US and China were optimistic and while relations between the two countries are better than six months ago there is a long way to go down that path.

- The US 10-year bond has declined by around 70 basis points in just over a month and from the recent highs of 5 % stands closer to 4.3 %. We have long felt the move up in yields was overextended as the tightening over the last twelve months would work its way through the system to produce a slowing effect on the economy.

- Inflation in Europe is coming off quicker than expected and one would expect the US to display a similar profile over the next quarters.

- With reporting season wrapping up we see continuing strength in earnings, relative to forecasts, despite sales being lacklustre. These numbers have challenged the overly bearish expectations of some prominent market strategists.

- As we head into the most illiquid month for market activity there is a decent chance that many investors who have not captured adequate gains will likely feel compelled to increase their exposure thus, leading to continued price appreciation.

- The spike in the VIX related to the Middle East tensions has dissipated and with the index at around 13 we are close to the lowest levels seen over the last ten years. We are tactical buyers of volatility at these levels.

The S&P 500 has its best November in decades

What’s not to like with the Federal Reserve easing off, the Middle East not escalating and volatility close to decade lows.

Key Markets

- Heading into 2023 all strategists and analysts expected a dismal start to the year. We correctly went against the grain and have benefitted from that stance. As December rolls around we will focus on understanding the analytical positioning of market participants and form a view for the first half of 2024. Early evidence suggests that opinions are more varied than last year and we will update on the same in our next update.

- India is a market that has participated well with the prevailing bullish mood. An on-the-ground assessment suggests that the Modi Government has set in motion programs that likely lead to a sustainable growth path. The latest quarterly GDP numbers show growth of 7.6 % from the prior year and ahead of market estimates of around 6.8 %. With important state election results to be declared in the coming days as well as a General Election in May 2024 there is ample scope for volatility should we see surprises. Having said that, we would use declines in valuations to build allocations to the Indian equity markets as the longer- term story appears positive.

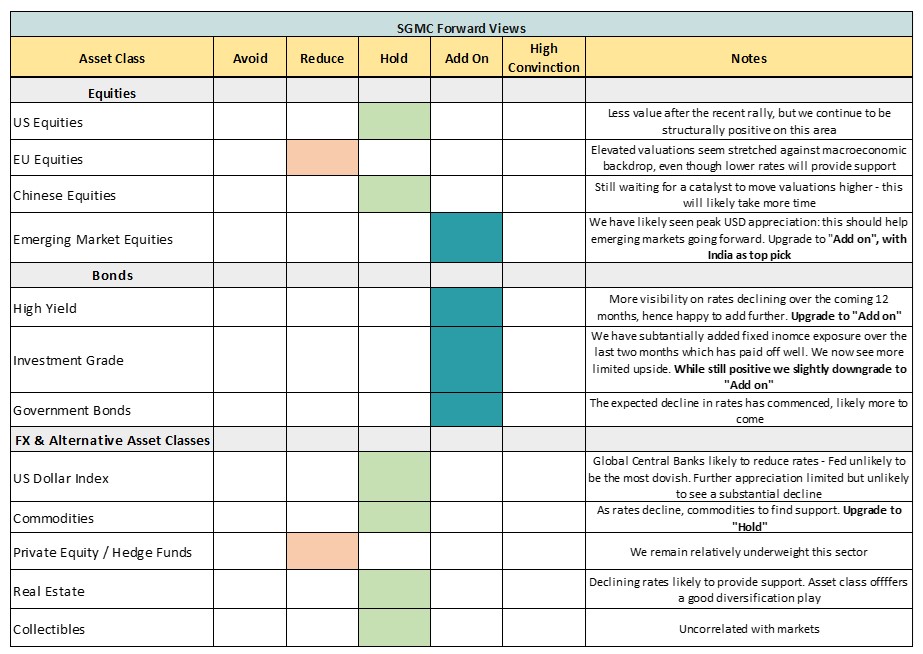

SGMC Forward Views …

- We upgraded Emerging Markets equities given the likely peak USD appreciation being behind us

- Overall we find this environment of likely declining global rates to be particularly interesting for fixed income and hence we are overweight across most sectors of the market. After the recent moves we feel Investment Grade bonds, while still attractive, now provide slightly lower relative value and we would thus be happy to increase credit risk, either via subordination or lower credit rating, to lock in higher yields