MONTHLY NEWSLETTER – MARCH 2026

April 1, 2026 |

Download Document

A summary of key events and market trends during the month of March

Global Markets Updates

- NVIDIA’s annual GPU Technology Conference, held March 10–14, marked a meaningful shift in tone from prior years. Rather than centering on hardware benchmarks and raw compute metrics, GTC 2026 was dominated by production deployment case studies and enterprise agentic frameworks — including NVIDIA’s NeMoCLAW, which was demonstrated running 47-agent pipelines handling end-to-end procurement workflows for a major manufacturing customer. The conference underscored that AI infrastructure conversations have moved decisively from the lab to the boardroom, with real operational deployments now setting the agenda. Nvidia’s dominance of the AI landscape and Jensen Huang’s portrayal of the company as an AI Factory is coming into sharp relief.

- The scale of AI’s commercial footprint came into view this month with new projections showing that AI-driven advertising is on course to grow 63% in 2026, reaching $57 billion and accounting for a significant share of total U.S. ad spend, as platforms that automate targeting, bidding, and campaign optimisation gain rapid adoption among both large and small advertisers. The numbers are a useful reminder that AI’s economic impact is not confined to technology companies — it is quietly restructuring the cost base and competitive dynamics of virtually every consumer-facing industry.

- March’s Federal Reserve meeting delivered no surprises on rates — but plenty of drama around everything else. The FOMC voted 11-1 to hold the benchmark federal funds rate at 3.50%–3.75%, as policymakers weighed stubborn inflation, a softening labour market, and the oil shock flowing from the Middle East conflict, which pushed crude above $100 per barrel and market pricing from two cuts this year down to one with a brief interlude of a hike too. Jerome Powell’s term expires in May, with Kevin Warsh — Trump’s preferred successor and a known rate-cut advocate — waiting in the wings.

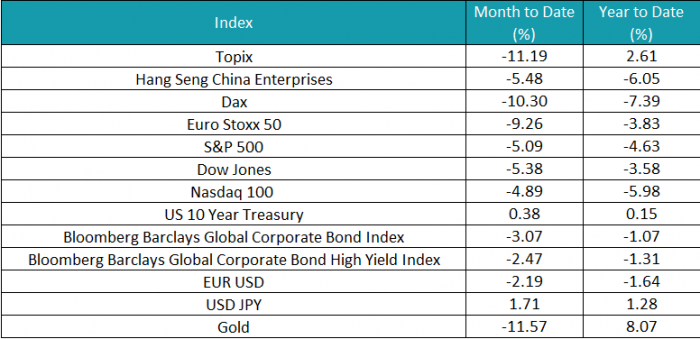

- Currency markets in March were shaped almost entirely by oil. EUR/USD fell roughly 4% as Europe’s structural energy dependence once again transformed a geopolitical supply shock into simultaneous pressure on its currency and sovereign spreads. The dollar found support as a net energy exporter. USD/JPY pressed toward the critical 160 level — twice defended by Japanese intervention in recent years — with the pair and oil futures trading at near-perfect correlation through the month, leaving Tokyo’s Ministry of Finance conspicuously watchful.

Geopolitical risk recedes?

March has been a turbulent month for global economies and markets with the core and determinative issue being the availability of crude oil.

The month has ended on a speculative note of optimism and the US stance on the way forward will drive markets in April.

Key Markets

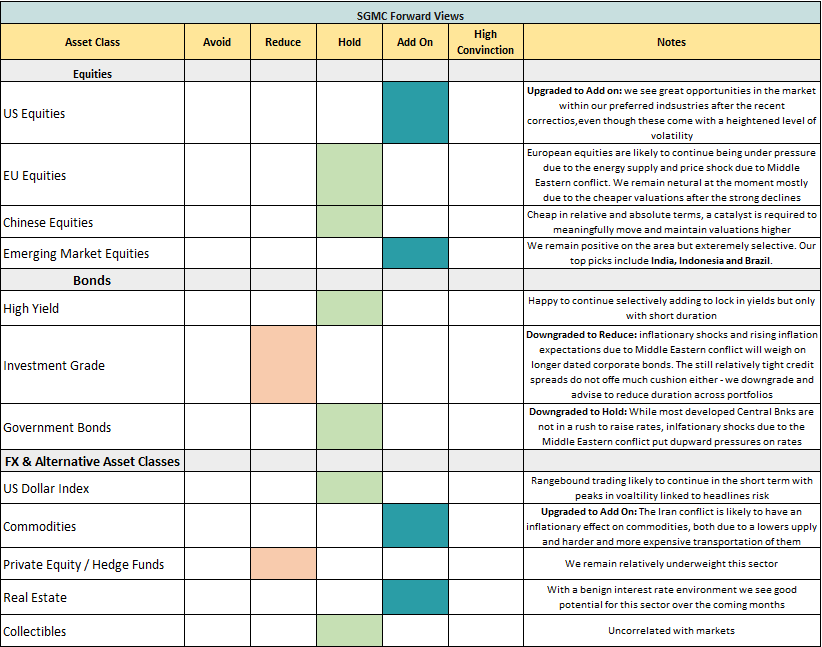

SGMC Forward Views …

- Upgraded US Equities from Hold to Add On: Despite the current negative headlines the US appears to be well positioned across global equity markets. Multiple drivers that we have focused on (mainly Reindustrialization & AI) will play out with likely a higher intensity in the coming months. Heading into the mid-term elections one would expect the upside momentum to continue, albeit with a higher volatility due to ongoing conflict.

- Downgraded Investment Grade and Government Bonds: inflationary shocks and rising inflation expectations due to Middle Eastern conflict will weigh on longer dated issues. We downgrade and advise to reduce duration across portfolios.

- Upgraded Commodities from Neutral to Add on: The Iran conflict is likely to have an inflationary effect on commodities, both due to a lower supply and harder and more expensive transportation of them.